Learning a Game by Paying the Agents

Apr 24, 2026

Learning to Play Multi-Follower Bayesian Stackelberg Games

Apr 23, 2026

Generalized Principal-Agent Problem with a Learning Agent

Please see the conference version of this work for details.

Jan 1, 2026

On the Coordination of Value-Maximizing Bidders

Nov 7, 2025

Generalized Principal-Agent Problem with a Learning Agent

Classic principal-agent problems such as Stackelberg games, contract design, and Bayesian persuasion, often assume that the agent is able to best respond to the principal’s committed strategy. We study repeated generalized principal-agent problems under the assumption that the principal does not have commitment power and the agent uses algorithms to learn to respond to the principal. We reduce this problem to a one-shot generalized principal-agent problem where the agent approximately best responds. Using this reduction, we show that: (1) If the agent uses contextual no-regret learning algorithms with regret $\mathrm{Reg}(T)$, then the principal can guarantee utility at least $U^* - \Theta\big(\sqrt{\tfrac{\mathrm{Reg}(T)}{T}}\big)$, where $U^*$ is the principal’s optimal utility in the classic model with a best-responding agent. (2) If the agent uses contextual no-swap-regret learning algorithms with swap-regret $\mathrm{SReg}(T)$, then the principal cannot obtain utility more than $U^* + O(\frac{\mathrm{SReg(T)}}{T})$. But (3) if the agent uses mean-based learning algorithms (which can be no-regret but not no-swap-regret), then the principal can sometimes do significantly better than $U^*$. These results not only refine previous results in Stackelberg games and contract design, but also lead to new results for Bayesian persuasion with a learning agent and all generalized principal-agent problems where the agent does not have private information.

Apr 24, 2025

Learning Thresholds with Latent Values and Censored Feedback

May 1, 2024

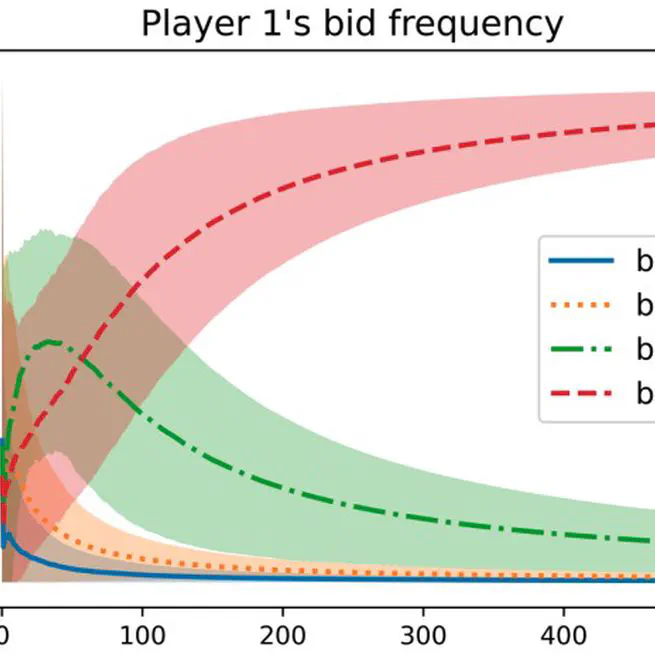

Nash Convergence of Mean-Based Learning Algorithms in First Price Auctions

The convergence properties of learning dynamics in repeated auctions is a timely and important question, with numerous applications in, e.g., online advertising markets. This work focuses on repeated first-price auctions where bidders with fixed values learn to bid using mean-based algorithms — a large class of online learning algorithms that include popular no-regret algorithms such as Multiplicative Weights Update and Follow the Perturbed Leader. We completely characterize the learning dynamics of mean-based algorithms, under two notions of convergence: (1) time-average: the fraction of rounds where bidders play a Nash equilibrium converges to 1; (2) last-iterate: the mixed strategy profile of bidders converges to a Nash equilibrium. Specifically, the results depend on the number of bidders with the highest value:

Apr 25, 2022