From Monopoly to Competition: Optimal Contests Prevail

Feb 1, 2023

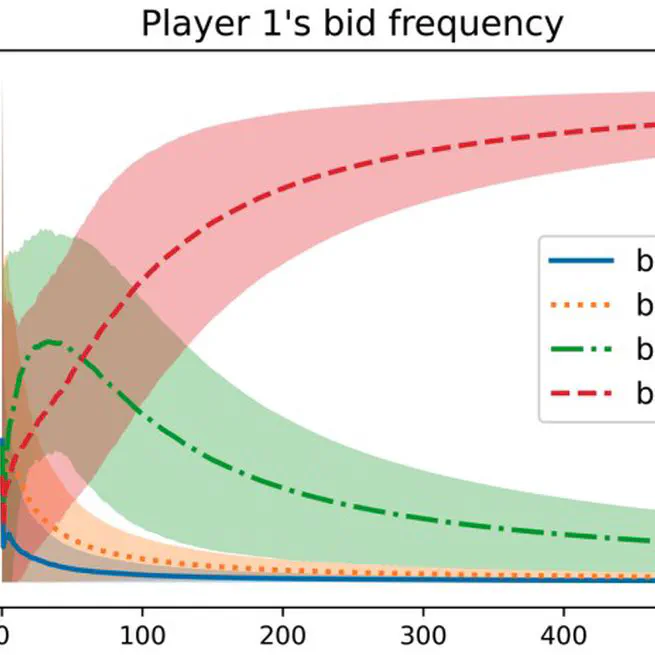

Nash Convergence of Mean-Based Learning Algorithms in First Price Auctions

The convergence properties of learning dynamics in repeated auctions is a timely and important question, with numerous applications in, e.g., online advertising markets. This work focuses on repeated first-price auctions where bidders with fixed values learn to bid using mean-based algorithms — a large class of online learning algorithms that include popular no-regret algorithms such as Multiplicative Weights Update and Follow the Perturbed Leader. We completely characterize the learning dynamics of mean-based algorithms, under two notions of convergence: (1) time-average: the fraction of rounds where bidders play a Nash equilibrium converges to 1; (2) last-iterate: the mixed strategy profile of bidders converges to a Nash equilibrium. Specifically, the results depend on the number of bidders with the highest value:

Apr 25, 2022

How Many Representatives Do We Need? The Optimal Size of a Congress Voting on Binary Issues

Feb 1, 2022

Learning Utilities and Equilibria in Non-Truthful Auctions

Dec 2, 2020

A Game-Theoretic Analysis of the Empirical Revenue Maximization Algorithm with Endogenous Sampling

Dec 1, 2020

Private Data Manipulation in Optimal Sponsored Search Auction

May 1, 2020

An example conference paper

Lorem ipsum dolor sit amet, consectetur adipiscing elit. Duis posuere tellus ac convallis placerat. Proin tincidunt magna sed ex sollicitudin condimentum.

Jul 1, 2013